The soft drink market in France

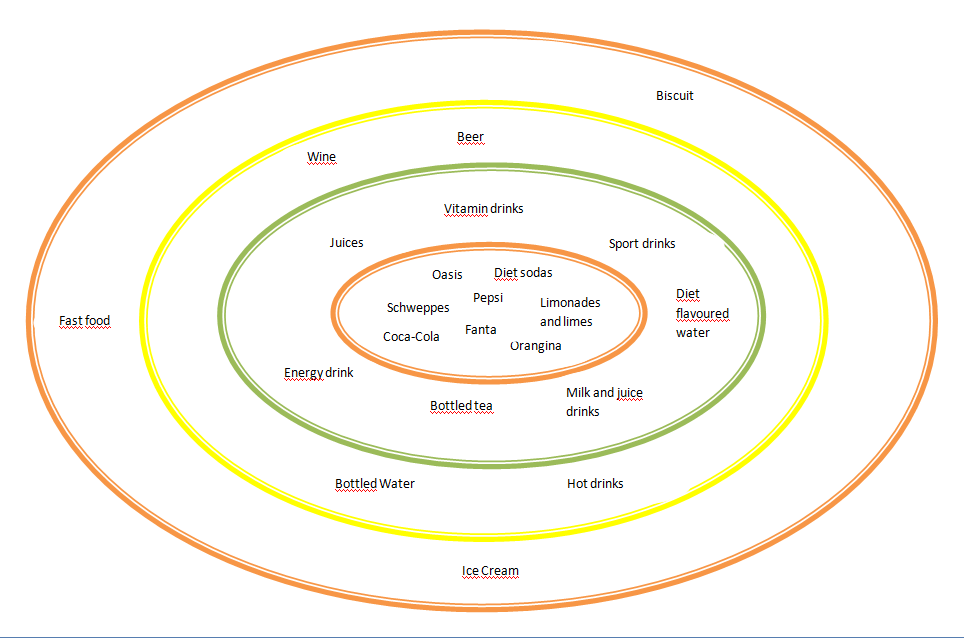

A soft drink is a beverage composed with a mix of water or carbonated water, sweetener – sugar, high-fructose corn syrup, fruit juice, and sugar substitutes – and a flavouring agent. It is a non-alcoholic beverage: “soft” drink by opposition to “hard” drink, an alcoholic beverage. It includes carbonated soft drinks, water, juices, bottle teas and more recently energy drinks.

A market valued at 2.3 bio Euros

Due to the recent crisis that affected French purchasing power, French consumption is cutting down. The Engel law asserting that the more wages are low the more important is the budget rate dedicated to the food industry is applied in the food-processing industry in France. Moreover, the implementation in 2012 of the sugar tax in France, in order to foster non-sugar drinks consumption caused soft drink industrials to increase their prices. Not to mention that the rise in raw material makes the tensions between retailers and industrials getting worse.

According to Nielson, d’après fabricants, the sales volume of soft drinks has cut down to 2.4% between January and May 2013. However, the soft drinks market variations with a value of 2.3 bio Euros, impact brands differently.

The competition in the soft drink market is getting bigger over the years

Indeed, from January to June 2013, the leader Coca-Cola steps back to 1.5 point with 53.4% of market shares; Orangina-Schweppes, second in the position ranking gains ground with 1 point to 17.6% as well as Pepsi, with 0.7 point to 6.3%. Cf. Appendix 1&2

Even if Coca-Cola is far ahead its competitors, other brands are gaining ground and hope to catch up with the Atlanta brand over the years. As a consequence, brands are developing their overall strategies and put the premium in marketing strategies using advertisements, internet buzz, or even increase their spending in Corporate Social Responsibility in order to give a sustainable aspect to their products.

Industry analysis

www.lefigaro.fr

wikipedia.org

By Sparkling Kiwi!

|

| Industry analysis |

- Sources:

www.lsa-conso.frwww.lefigaro.fr

wikipedia.org